How Innovation, Invention, and Improvement Differ in BFSI—And How Banks Should Prioritize Each Under Risk and Compliance

Blog Summary

Innovation in BFSI is not just about following rules and regulations while advancing in an industry. Innovation in BFSI involves invention, bringing newly created ideas to market, and improvement, enhancing the status quo. We can employ design thinking and behavioural science in selecting the optimal innovative pathway.

Introduction

The banking sector finds itself at a crossroads with a daunting task in balancing innovation with risk management in a sluggish environment fraught with regulatory imperatives. With technology emerging as the game changer in the banking sector, there is the increasing need to keep pace with the rapid change occurring in the marketplace and the evolving needs of the customers. Banks face a challenging and often unproductive exercise in managing risk in a slow moving environment fraught with the imperatives of regulatory and compliance risks.

There is a difference between invention, innovation and improvements to the current service model and all three offer various trade-offs between risk and reward. Understanding the model best suited to advance your business goals is therefore essential to your future success. Deloitte research also confirms that the costs associated with banks’ efforts to comply with new regulations have increased by an average of 60% since 2008. However, sound banking practice requires that banks balance progress with sound risk management.

What Do Invention, Innovation, and Improvement Mean?

Invention: Creating Something Newy

Invention is often defined as the construction of something that has never existed before. It is born of an original idea.

Key traits:

- Totally new concept

- High risk

- Needs major research money

- Takes 3-5+ years

The ATM in the 1960s was an invention that changed the way people withdrew money from bank. Blockchain is another invention that will change the way money is moved, in the same way.

Innovation: Making Ideas Work

At Money20/20, the future of innovation in BFSI was clear: Innovation in BFSI is about using technology to solve real problems.

Key traits:

- Uses ideas to create value

- Medium to high risk

- Needs building and marketing

- Takes 1-3 years

Innovation Example: Mobile Banking Apps- How the Combination of Existing Technologies Transformed Customer Banking?

Mobile banking apps are a classic example of banking innovation. Smartphones existed and the Internet connectivity was in place. All the banks had to do was to connect the two to create simple mobile apps that were soon to change the way customers banked!

Improvement: Making Things Better

The role of improvement is to fix the way things are done currently, to make them faster and easier.

Key traits:

- Builds on proven ideas

- Low risk

- Shows quick results

- Works in weeks or months

A real world example of this in action is high street Banks such as LloydsTSB, Barclays and the rest of them, reducing the time taken to approve loans from weeks to just days. They have refactored their internal business processes, in essence improving and speeding up the very same loan system that were using before.

How Do These Three Compare?

Why Do Risk and Compliance Matter?

Banking is a heavily regulated business. Capital requirements are dictated by Basel III. Customer data must be protected from GDPR invaders. Due diligence is necessary for AML/KYC checks. These requirements have the effect of instilling fear in bankers. Innovative and bold actions are put on hold as bankers are loathe to take risks that could be punished with hefty fines.

Rules and innovation can sometimes be at odds. But smart banks make rules and innovation work better together. Most adopt what we call “compliance by design”. This means that rules are embedded into the product and service early on, which in turn accelerates the approval process and reduces the need for subsequent fixes.

How Does Design Thinking Help Banks?

Design thinking is customer focused. It starts by asking: What problems does our customer need to solve? Not: What can we build?

The Five Steps

Empathize: Study customer needs

Define: State the problem clearly

Ideate: Create many solutions

Prototype: Build simple test versions

Test: Get feedback and improve

Instead of coming at it from the angle of "sell more credit cards" ask yourself, "How can we help young people manage their cash flow better?" - a completely different approach.

Involve compliance teams early in the design process to catch any potential rule violations, saving time and money late in the design cycle.

How Does Behavioral Science Help?

Understand how people will behave. Behavioral science shows why people choose what they do.

Loss Aversion: Kahneman found that in general people fear loss more than they value gain. Loss aversion coefficients typically come out to around 2, meaning that the pain of losing a dollar is equal to the pleasure of gaining two. But bank bosses don't want to lose a million dollars to only avoid a loss of a million dollars of their bank's capital. Knowing this bias is half the battle. Present your offer in terms of gain, rather than loss.

The Herd Mentality: Banks copy rivals when it makes no sense. But once they see another bank has done something, they then proceed to do it badly. Don’t just copy what another bank has done. Think.

Confirmation Bias: We see facts that support our views, ignore those that don’t. Banks often reject great partners because they are a threat to the status quo. But let’s look at the data and the facts.

These ideas can be useful when selecting bank services, and more broadly designing customer experiences.

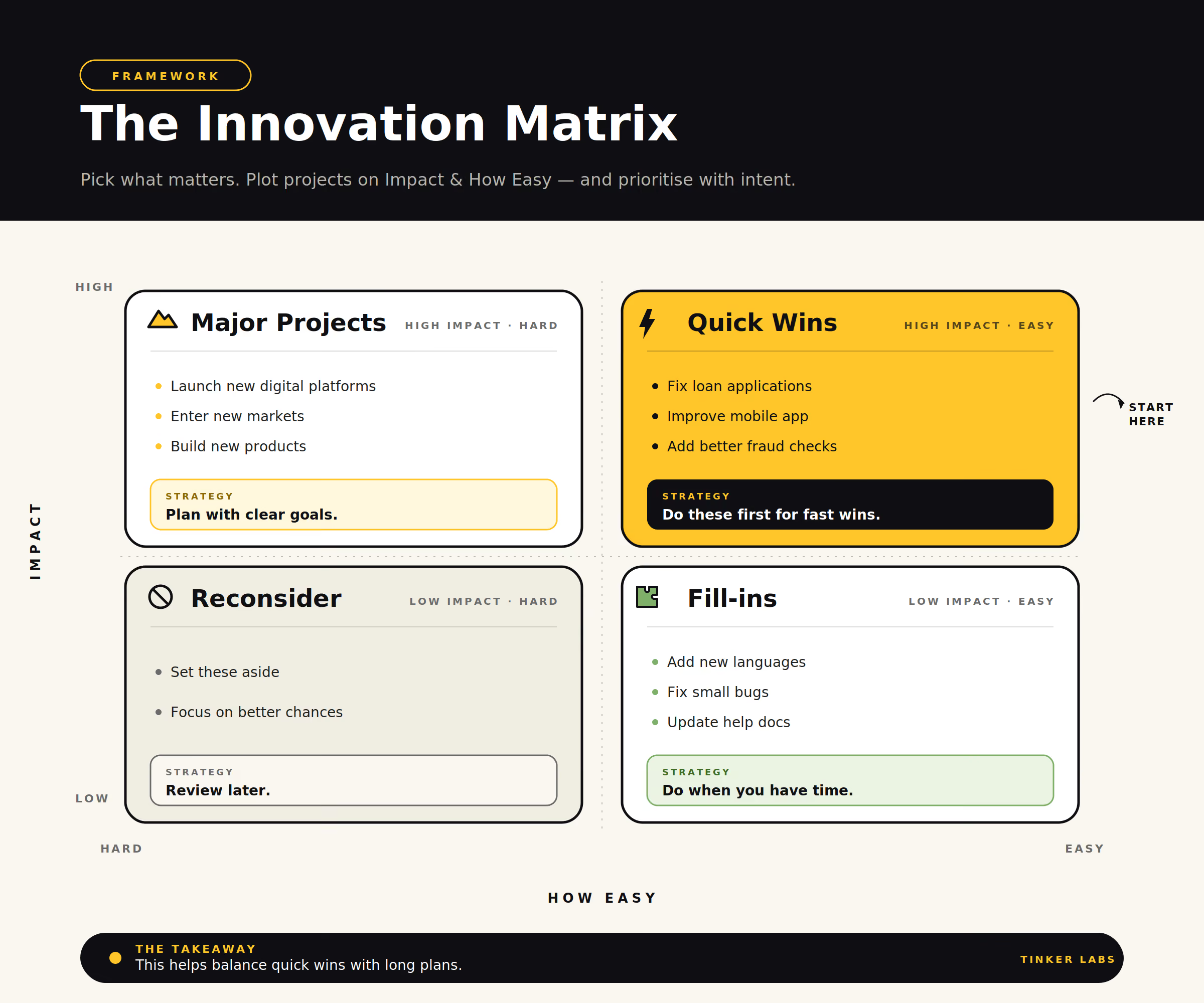

The Innovation Matrix: Pick What Matters

Banks select projects they fund. Criteria for this selection can be quite complex; using the two highlighted criteria can simplify the process and provide effective bank wide prioritization of investment opportunities.

Four Types of Projects

Quick Wins (High Impact, Easy):

- Fix loan applications

- Improve mobile app

- Add better fraud checks

- Do these first for fast wins

Major Projects (High Impact, Hard):

- Launch new digital platforms

- Enter new markets

- Build new products

- Plan with clear goals

Fill-ins (Low Impact, Easy):

- Add new languages

- Fix small bugs

- Update help docs

- Do when you have time

Reconsider (Low Impact, Hard):

- Set these aside

- Focus on better chances

- Review later

This helps balance quick wins with long plans.

How Can Banks Build Innovation Culture?

Step 1: Make It Safe to Try

Hold safe space for ideas to be tested and take risks. Celebrate smart failures. Leadership can change the culture from a place of blame to a culture of learning.

Step 2: Build Mixed Teams

Bring together product, tech, marketing, legal and compliance teams early in the process. They have different perspectives which will generate better answers and expose any potential risks earlier.

Step 3: Know Your Customers

Most organizations use surveys to better understand customer needs. Taking it a step further, organizations can watch customers using their services and learn about their money worries. Innovators learn a lot by hearing these types of concerns.

Step 4: Balance Your Work

Use this simple matrix to prioritize projects. Spread risk by combining improvements, innovations, and inventions.

Step 5: Track and Learn

Establish targets. Assess what works and what doesn't. Learn and improve.

Closing Thought

Innovation in banking is not a zero-sum game – banks don’t have to choose between testing new ground and preserving the assets they have. Knowing when to invent, when to innovate and when to improve what you already do is far more important and requires a different approach. By bringing design thinking to the customer understanding brief and behavioural science to the choice architecture brief, banks can draw on new skills to develop better solutions for customers and for the bottom line. Understanding the benefits early on, is creating products and services that are compliant by design.

The future of banking belongs to institutions that comply with regulations but also address real needs of people and businesses.

FAQ

While often used interchangeably, innovation and invention in banking have distinct meanings. Invention is about creating something entirely novel. In banking, invention involves introducing entirely new products and services that had previously not existed.

Invention is about inventing new concepts and technologies, like ATMs or block chain, whereas innovation is applying existing technologies to create offerings which people are willing to pay for, such as mobile banking apps. Banks need to be more innovative than in pursuing new technologies to invent. And while creating real innovation requires effort and risk, the potential payoff is greater than it is for invention, which takes a long time and typically emerges from a lab rather than from the mainstream of a bank. Therefore most banks would benefit from focusing more on innovation and less on invention.

What are some innovative practices that banks can follow in order to stay compliant?

Design compliance into products and services “by design”. Involve compliance teams early in the product design process. By addressing any rule issues at this early stage, you will be able to speed up the approval process, save money and innovate more quickly and safely.

Why is behavioral science important for banking innovation?

Behavioural science looks at how customers make money decisions. Understanding these biases can help banks and other financial organisations design financial products for customers. The key biases that affect how we make decisions are: loss aversion, herd mentality, confirmation bias. Knowing how these biases affect how customers act can help bosses make some smarter financial decisions. Knowing that customers stick with defaults can help the design of savings programs that are actually used.

Should banks prioritize improvement over innovation?

Banks should focus on making things better above all, with innovation as a secondary objective with faster and more reliable payoffs. We have found that the banks that excel are those that have focused on improving their core activities. If you do choose to innovate, you should only do so if you believe there is a real opportunity with genuine potential and a reasonable chance of success. If you are going to try to invent something entirely new then you need to have the requisite resources and be convinced that there is a meaningful gap in the market waiting to be filled.

What is the Innovation Prioritization Matrix and how does it work?

The matrix plots the ideas against two dimensions: Impact and How Easy it will be to do. It produces four boxes. Those on the upper left will be your Quick Wins - they have both High Impact and are Easy to deliver. The upper right-hand box represents your Major Projects - these have huge Impact but will be harder to complete. The lower left will be your Fill-ins - these have Low Impact but are easy to do and can 'fill in the gaps' for your priorities. The lower right will be your Reconsider Options - these have both Low Impact and are hard to deliver. The prioritisation tool helps to get a healthy mix of all types of projects to deliver both quick wins and longer-term strategic objectives.

References

Deloitte. Financial Services Regulatory Outlook. Deloitte Web site. Published Jan 2026. Available at: Global foreword

Kahneman D. Thinking, Fast and Slow. Farrar, Straus and Giroux; 2011. Available from: Thinking, Fast and Slow

R. H. Thaler, C. R. Nudge: https://www.penguinrandomhouse.com/books/690485/nudge-by-richard-h-thaler-and-cass-r-sunstein/. Accessed Jan 2026.

Basel Committee on Banking Supervision. Basel III: International regulatory framework for banks. Bank for International Settlements. Available from: Basel III: international regulatory framework for banks. [Accessed Jan 2026].

About the Author

Mandeep Toor

Head of Trainings & Workshops at Tinker Labs

Mandeep helps organisations build innovation capability through design thinking and behavioural science. With over a decade in innovation and entrepreneurship, he has led 75+ workshops for leaders at firms like Piramal Group, Samsung, Flipkart, HP, and Hindustan Unilever, and teaches Design Thinking at IIMs, MICA, and SOIL Institute of Management. Know more →

About TinkerLabs

Tinker Labs helps organizations use design thinking and behavioural science for innovation challenges. We believe successful innovations come from understanding human behavior. We design solutions that work with human nature. Whether you pursue invention, innovation, or improvement, we help you make smart choices, test faster, and scale with confidence.

For more insights, visit tinkerlabs.in